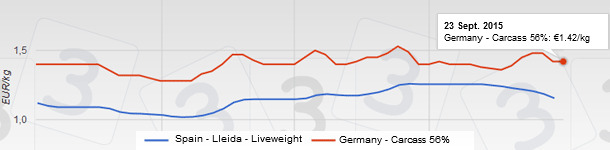

In September, just as we foresaw in our previous analysis, the Spanish price has fallen week by week. Let us look at the following comparative chart:

| German market (€cents / kg carcass) |

Mercolleida, Spain ( €cents/ kg liveweight) |

|

| 4th week August | + 3 | - 1.3 |

| 1st week September | + 6 | - 1.0 |

| 2nd week September | + 3 | - 1.2 |

| 3rd week September | repetition | - 2.0 |

| 4th week September | - 6 | - 3.0 |

| Current week | repetition | - 3.1 |

The Spanish price reached an European record by the end of August, at a much higher level than all our competitors. The German blow of + 12 €cents in three weeks has been useful to bridge the gap (we are still a step ahead), and although the Germans have lost strenght, the differences have been reduced.

In our market, Mother Nature is imposing her law (this is nothing new, because every year the market has a similar behaviour in autumn). The pigs welcome the mild weather and grow quickly.

The current reality is that there is a plentiful supply in Spain, just as in the rest of Europe; Russia is still closed; the exports to third countries (mainly Asia) are higher than ever, and the abattoirs are fighting hard to sell their meat. Globalisation is the word. Competitiveness and competency are the concepts.

We are in a downward price curve and we will still be in it for some more weeks.

The farmer needs the slaughterings to be very flowing, and lowering the price is the only stimulus that encourages slaughterings. This is the situation we are in.

We think that in October the price will still fall. We do not not at which pace. With the end of the summer and the tourists back in their homelands, Spain cannot keep its price on a pedestal, losing touch with the European reality. A correction for the alignment with our neighbours is prevailing.

As W. Steitnitz (considered as the first chess world champion) once said: "The player that has an advantage must attack, or it will lose this advantage".

Guillem Burset