June began with the news that Vion was abandoning its slaughter and cutting activities in Germany. This marks the end of the Germanic adventure of this cooperative of Dutch cooperatives. Vion still has a few remaining slaughterhouses in Germany, which, for the time being, are for sale.

The slaughtering and cutting sector in Germany has changed substantially in just a few years. Several plants have closed down as an inevitable consequence of the sharp decrease of the herd in the Teutonic country. The position of the leader, Tönnies, has been strengthened by the departure of its most significant competitors. This operator's current pre-eminence is beyond doubt.

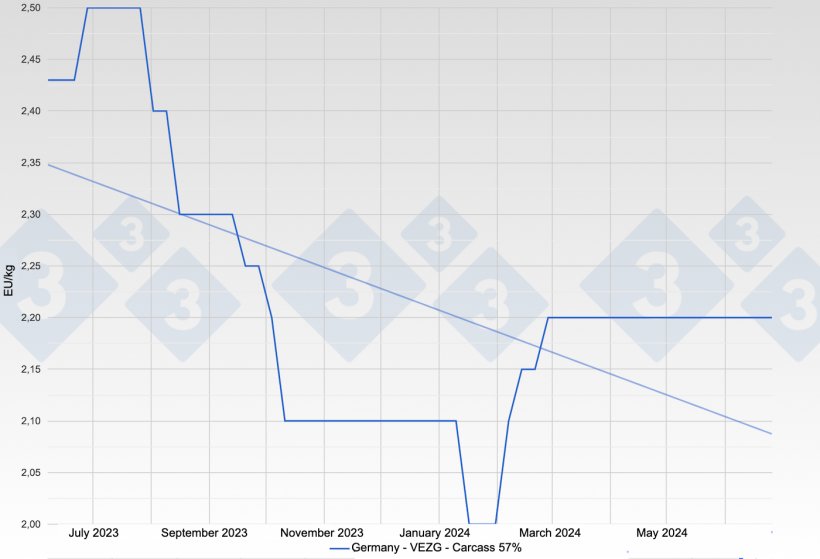

To complicate matters further in Germany, we have learned of the appearance of some African swine fever (ASF) cases on domestic pig farms (after a few years of cases only in wild boars). This circumstance has caused the sporadic halt of some slaughtering plants and serious problems in German exports to third countries, which were already very penalized. Germany's pig price remained unchanged in the last market session of the month, which means that the price has stayed the same for 17 weeks (a third of a year!) in an admirable exercise of unstable equilibrium.

Without a doubt, the big news in June has been the possible retaliation by China against EU pork exports (there is talk of introducing taxes or duties). This would be a measure to compensate for the EU's decision to increase tariffs on electric vehicles from China. Any limitation on the flow of pork from the EU to China is very negative, there is no doubt about that. China has been the main destination for our exports for several years and continues to be the main and most important buyer of our offal and viscera. The absence of this market would directly and immediately affect the results of the Spanish slaughter and cutting industry. Great concern is really being felt in the slaughterhouses in this regard: without China as a destination, it would be very unclear what to do with some by-products, which would hinder pricing. The fact that cured hams and other sausages will be spared from these potential new tariffs is completely trivial if we consider the nature of the volumes exported to China.

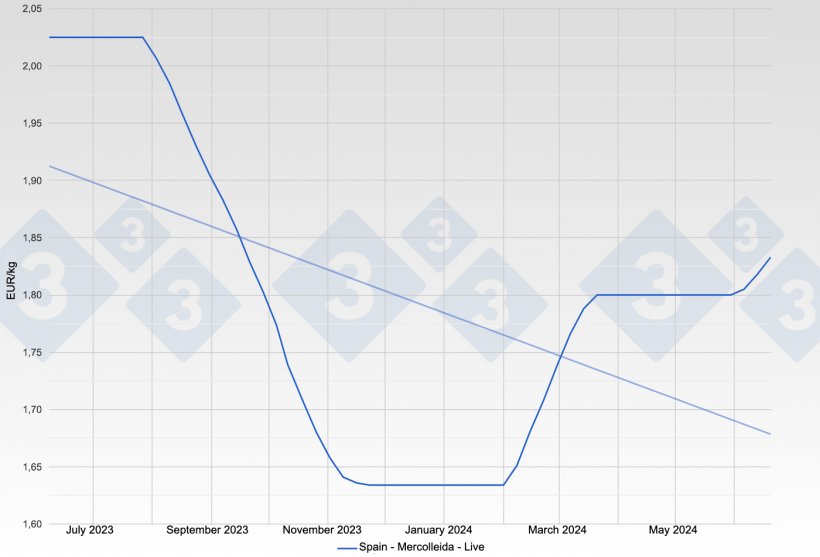

In the Spanish market, June began with breaking the inertia of 10 repeat market sessions. The consecutive increases make logical sense for the season; in a rather depressed pork market, the price increases are supported by the supply restrictions typical for June. As is the case every year, the heat will be a great ally to Spanish pig farmers. Will it be enough to keep prices up there until September? We have our doubts. The modest increases and the braking seen in the last session (1.10 cents when a week ago it had risen 1.50) seem to indicate that we are very close to the upper limit.

Figure 2. Evolution of the pig price in Spain - Mercolleida - Live.

With a seemingly firm pig price and a rather depressed pork market, we get the feeling July will be complicated. With the Great Export more than stagnant - with the honorable exception of bellies - due to the unbeatable American competition (Brazil and the United States) and European consumption in clear decline, the available pork is definitely more than enough. The celebration of the European Football Championship in Germany has not stimulated consumption in any way. This is the harsh reality. Nobody wants to freeze at these prices and they try to sell fresh. Spanish slaughterhouses' margins are weakening little by little because it is impossible to transfer the increases in the live price to the pork. We think the current bottleneck in the pork trade will not allow much excitement in the hog price increase.

We have crossed the midpoint of the year. For the Spanish farmers it is turning out to be an extraordinary year with pig prices well above the cost price; for the slaughterers it is turning out to be better than last year because the live price has not been pushed to the limit and they have been able to do better than in other years. For the charcuterie industry, the eternal ordeal continues, with the sale prices of their processed products lagging far behind pork prices.

Under normal conditions, it seems to us that the pig price in Spain should reach its annual maximum in July. Once we have reached the year's zenith, it will be a question of how long the high can be maintained. We are at an advantage over other countries where ASF is. Let's keep our fingers crossed. We will see.

We will end with a concise quote from Gandhi: "It is unwise to be too sure of one's own wisdom or strength. It is healthy to be reminded that the strongest might weaken and the wisest might err."

Guillem Burset